Browse By Unit

Unit 1 Overview: Basic Economic concepts

3 min read•june 18, 2024

Isabela Padilha

Isabela Padilha

Unit 1 Overview: Basic Economic concepts

To start your study of Economics it is important to understand what the Economic system is about. In this course, Economics is understood as the systematic study of choice. 🧐 Another way to think about it is to consider that individuals have wants and needs in a world that has limited resources 🌏. Economics studies the allocation of those based on individual choices.

The purpose of this unit is to introduce you to the skills 🔨 you will need to use until the end of the course. Before jumping right into these crucial concepts, it is important to keep these macroeconomic 🤑 questions in mind:

-

Why do people and countries trade with one another?

-

What determines the market price for a good service?

Both of these questions can be answered through the study of markets, which exist in an ideal accord with the 19th Century concept of laissez-faire. In a "free market" world, ideally, resources are allocated perfectly. This philosophy has extremely shaped modern capitalism as we know it. 💭

Introduction to crucial concepts:

1. Scarcity 🍽: Refers to the limitation of any physical resource, such as raw materials or food. It may also be "intangible," such as time 🕐. It is the big dilemma of Economics, since humans have unlimited wants in a world where resources are finite.

You cannot solve the problem of scarcity, only allocate resources in different ways.

2. Opportunity Cost and the Possibilities Curve : Have you ever heard the saying "there is no free lunch?" 🌮 It stems from the idea of opportunity cost, which refers to the value of the next best alternative that must be given up in order to pursue a certain action/goal.

The possibility curve illustrates in an economy what are the limitations of what can be produced. It is important to remember that the PPC (Production Possibility Curve) will consider that all resources are being fully employed.

(Always remember: when graphing, you will always have to label the axis!)

3. Comparative Advantage 📊: It is the possibility of an economic actor (a country, firm or individual) to produce a good at a lower opportunity cost than its competitor. It is a concept developed by David Ricardo in the 19th Century and it still highly influences modern capitalism. You will learn more on how to identify who has a comparative advantage later in this unit.

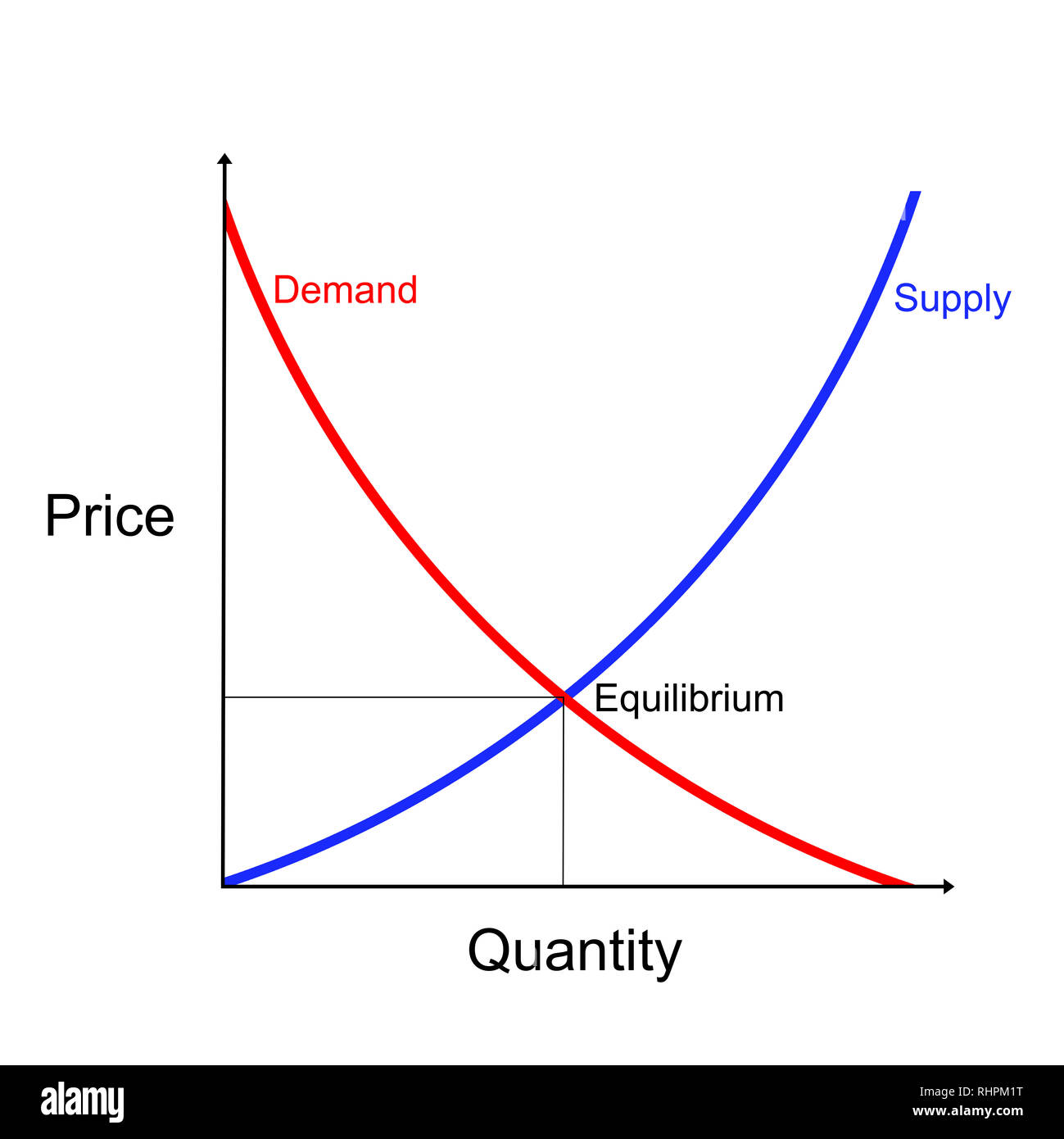

4. Demand 📉 and Supply 📈 : It refers to the quantity of a good or service that the consumers are willing to purchase at a certain time. Supply, on the other hand, represent a quantiy of a good and service that an economic actor is able to provide at a specific period of time. Both of these influence how much of a good is produced. You will learn how to graph both a supply and demand curve in this unit.

5. Equilibrium ⚖️: This concept is highly related to the ideas of supply and demand. Basically, an economy is considered to be at "equilibrium" when the quantity supplied equals to the quantity demanded. The ultimate goal in a market is to reach the equilibrium point. You will later learn about all the implications of equilibrium on the producer and consumer behavior. 🧠

<< Hide Menu

Unit 1 Overview: Basic Economic concepts

3 min read•june 18, 2024

Isabela Padilha

Isabela Padilha

Unit 1 Overview: Basic Economic concepts

To start your study of Economics it is important to understand what the Economic system is about. In this course, Economics is understood as the systematic study of choice. 🧐 Another way to think about it is to consider that individuals have wants and needs in a world that has limited resources 🌏. Economics studies the allocation of those based on individual choices.

The purpose of this unit is to introduce you to the skills 🔨 you will need to use until the end of the course. Before jumping right into these crucial concepts, it is important to keep these macroeconomic 🤑 questions in mind:

-

Why do people and countries trade with one another?

-

What determines the market price for a good service?

Both of these questions can be answered through the study of markets, which exist in an ideal accord with the 19th Century concept of laissez-faire. In a "free market" world, ideally, resources are allocated perfectly. This philosophy has extremely shaped modern capitalism as we know it. 💭

Introduction to crucial concepts:

1. Scarcity 🍽: Refers to the limitation of any physical resource, such as raw materials or food. It may also be "intangible," such as time 🕐. It is the big dilemma of Economics, since humans have unlimited wants in a world where resources are finite.

You cannot solve the problem of scarcity, only allocate resources in different ways.

2. Opportunity Cost and the Possibilities Curve : Have you ever heard the saying "there is no free lunch?" 🌮 It stems from the idea of opportunity cost, which refers to the value of the next best alternative that must be given up in order to pursue a certain action/goal.

The possibility curve illustrates in an economy what are the limitations of what can be produced. It is important to remember that the PPC (Production Possibility Curve) will consider that all resources are being fully employed.

(Always remember: when graphing, you will always have to label the axis!)

3. Comparative Advantage 📊: It is the possibility of an economic actor (a country, firm or individual) to produce a good at a lower opportunity cost than its competitor. It is a concept developed by David Ricardo in the 19th Century and it still highly influences modern capitalism. You will learn more on how to identify who has a comparative advantage later in this unit.

4. Demand 📉 and Supply 📈 : It refers to the quantity of a good or service that the consumers are willing to purchase at a certain time. Supply, on the other hand, represent a quantiy of a good and service that an economic actor is able to provide at a specific period of time. Both of these influence how much of a good is produced. You will learn how to graph both a supply and demand curve in this unit.

5. Equilibrium ⚖️: This concept is highly related to the ideas of supply and demand. Basically, an economy is considered to be at "equilibrium" when the quantity supplied equals to the quantity demanded. The ultimate goal in a market is to reach the equilibrium point. You will later learn about all the implications of equilibrium on the producer and consumer behavior. 🧠

© 2024 Fiveable Inc. All rights reserved.